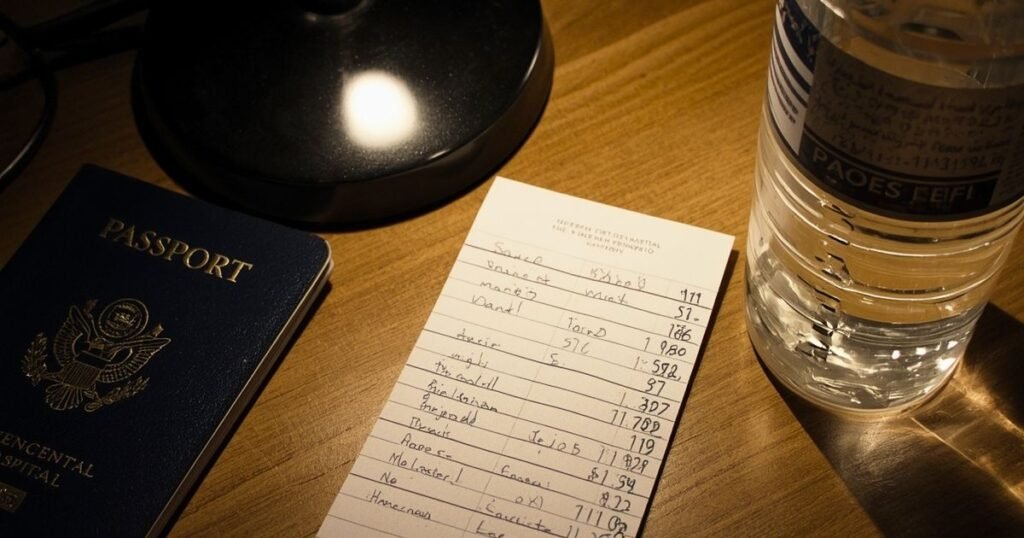

I almost skipped SafetyWing for solo travel on my first trip. I was 28, broke, and thought “what is really going to happen?” Then I got food poisoning in Vietnam, spent 6 hours in a clinic in Hanoi, and paid $340 out of pocket because I was too cheap to buy a $45 policy. That was my entire hostel budget for two weeks.

Now I use SafetyWing for every trip. Here is why after five years of solo travel.

The Problem with Most Travel Insurance

Most plans are built for vacationers. They want your exact dates, your exact countries, your exact return flight. Change your mind and stay an extra month? Too bad. Already left home and forgot to buy it? Too bad. Want to extend from a beach in Bali? Definitely too bad.

That is not how solo travel works. Solo travel is messy. You meet someone and decide to go to a different island. You find a job and stay two extra months. You book a one way ticket because you do not know when you are coming home.

SafetyWing is the only plan I have found that actually works the way solo travelers actually travel.

What SafetyWing Actually Covers

Medical coverage up to $250,000. That sounds like a lot because it is. Hospital bills in foreign countries can destroy you financially. I have never needed that much but I sleep better knowing it is there.

You can start it while already traveling. Forgot to buy before you left? I have done this. You can sign up from anywhere with wifi.

Extend month by month. No set return date required. I have extended four times on the same trip. Takes 2 minutes.

Works in 180 countries. I have used it in Thailand, Portugal, Mexico, Japan. Never had a problem.

About $45 per month. That is less than I spend on coffee in a week.

How It Compares to What Everyone Else Uses

I used World Nomads on my second trip. It was fine until I wanted to stay longer. They needed a return flight to extend. I did not have one. I ended up buying a throwaway ticket just to keep coverage. That cost me $180.

HeyMondo is cheaper for short trips but gets expensive fast if you extend. IMG has better medical limits but requires you to buy before you leave. If you are already in Bangkok and realize you need insurance, they will not help you.

Here is how they stack up for the way I actually travel:

| SafetyWing | World Nomads | HeyMondo | |

|---|---|---|---|

| Monthly cost | ~$45 | ~$120–150 | ~$35–60 |

| Can buy while traveling | Yes | No | No |

| Extend without return flight | Yes | No | Limited |

| Home country coverage | 15 days every 90 | None | None |

| Adventure sports | Limited | Better | Limited |

I am not saying SafetyWing wins on everything. If you are doing a two week vacation and know your dates, World Nomads might be better. If you want the cheapest possible short trip, HeyMondo works. But for open ended travel with no plan? SafetyWing is the only one that does not punish you for being flexible.

What It Does Not Cover (Be Honest About This)

I am not going to pretend it is perfect. Adventure coverage is limited. Hiking and snorkeling are fine. Scuba below 30 meters, skydiving, motocross, and skiing off piste are not covered. Gear coverage is minimal. If you are bringing a $3,000 camera, you might want extra protection.

I treat it as my medical and emergency backbone, not my everything plan. For hiking, surfing, or motorcycle trips, I buy additional adventure coverage separately. For my laptop and phone, I just accept the risk.

If you need comprehensive adventure coverage or you are over 65, SafetyWing might not be enough. For everyone else doing standard backpacking, city hopping, or long term travel, it is exactly what you need.

How I Actually Use It

I sign up the day I book my first flight. Takes 5 minutes. No paperwork. No medical exam. No printing documents I will lose.

If I extend my trip, I get an email reminder before my month ends. I click one button. Done.

I have never filed a major claim but I have called their support twice. Once from a pharmacy in Chiang Mai because I could not read medication labels. Once because I was not sure if a clinic visit was covered. Both times I talked to a human in English within 2 minutes. That matters at 2 AM when you are alone and slightly panicking.

The One Time I Almost Needed to Use It

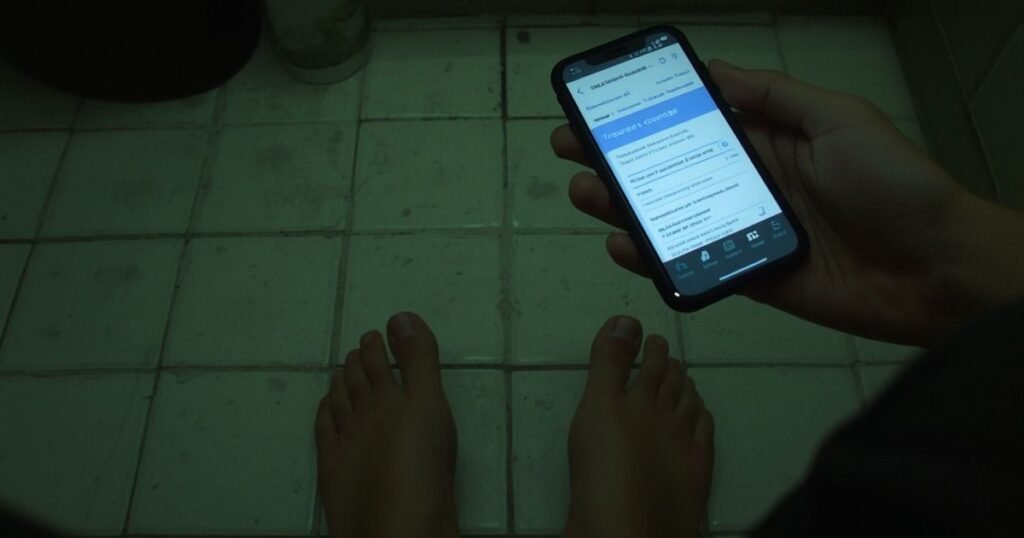

I was in Lisbon last spring. Woke up at 4 AM with chest tightness and could not breathe right. I was alone in a hostel room with six strangers asleep around me. I sat on the bathroom floor for an hour trying to decide if it was anxiety or something worse.

I did not go to the hospital. It was anxiety. But I checked my SafetyWing coverage at 4:30 AM while sitting on that tile floor. I knew the nearest hospital was covered. I knew I would not have to pay upfront. I knew the number to call if I needed help in English.

That is the real value. Not the claims you file. The 4 AM certainty that you are not going to be ruined by a hospital bill in a country where you do not speak the language. I fell back asleep on that bathroom floor because I knew I had a backup plan. That is worth $45 to me.

What Happens If You Actually Need to Claim

This is the part everyone skips because it is boring. I am going to tell you anyway because it is the only part that matters when you are sick.

You log into your account. You fill out a one page form. You upload photos of receipts and any doctor notes. You submit it. They say most claims process in 7–10 days. I have not done this myself but two people I met in hostels have. One got reimbursed for a clinic visit in Lisbon in nine days. The other got a $1,200 hospital bill in Bali paid in two weeks. Both said it was easier than they expected.

The deductible is $250. That means you pay the first $250 of any claim. For a $340 food poisoning clinic visit, that means you are still out of pocket $250. This is why I call it a backbone, not a everything plan. It is for the big stuff. The $5,000 appendectomy. The $20,000 evacuation. Not the $80 pharmacy run.

Who Should Not Use SafetyWing

I have been honest about what it does not cover. I should also be honest about who should look somewhere else.

If you are traveling with a family of four, SafetyWing charges per person. A family plan from Allianz or IMG might be cheaper overall. If you are on a organized tour with fixed dates, you do not need month-by-month flexibility. You are paying for something you will not use.

If you have serious pre-existing conditions, read the fine print. SafetyWing covers acute onset of pre-existing conditions up to a limit. It does not cover ongoing treatment. If you need regular medication or monitoring, this is not your plan.

If you are American and your main worry is getting home for treatment, SafetyWing only covers 15 days in your home country every 90 days. That is enough for a visit. It is not enough for a relocation.

I am not loyal to SafetyWing as a brand. I am loyal to what works for my specific trip. Right now that is open-ended solo travel with no plan. If that changes, I will change my insurance. You should too.

In conclusion

Travel insurance is boring. It is the least exciting purchase of your entire trip. It is also the one you will be most grateful for at 3 AM in a foreign emergency room, alone, trying to figure out if you can afford treatment.

SafetyWing is not fancy. It is cheap, flexible, and works everywhere. That is exactly what solo travelers actually need.

Get covered before you need it. Then forget about it and enjoy your trip.

Travel insurance protects you from medical bills. It does not protect you from fake taxi meters, rigged ATMs, or “free” tours that end in a souvenir shop. Here is what I learned about avoiding scams the hard way: How to Avoid Travel Scams as a First Time Traveler.

This post contains an affiliate link. I have used SafetyWing for years and only recommend what I actually pay for myself. If you sign up through my link, I earn a small commission at no extra cost to you. This helps me keep writing free guides for solo travelers.